How the Housing Market For Young People Became ‘A Total Disaster’

Donald Trump's scarcity agenda is not going to solve the problem. Here's what might.

Thanks for reading! If you’ve read ABUNDANCE, the book—or if you’ve just heard about it and want to know more—consider becoming a subscriber to this newsletter to receive more essays on building out the Abundance Agenda in housing, energy, health care, education, and beyond.

I do not often find myself listening to Tucker Carlson1 while nodding along with an enthusiasm that puts me at risk of neck injury. But that’s what happened earlier this week, as I listened to Carlson at a conservative conference describing the US housing market for young buyers.

It’s especially bad that young people can’t afford homes. If you want a measure of how your economy is doing ... My measure is really simple: I’ve got a bunch of kids. Can they afford a house with full-time jobs at 27, 28 years old? And the answer is: No way. Thirty-five-year-olds with really good jobs can't afford a house unless they stretch and go deep into debt. And I just think that's a total disaster.

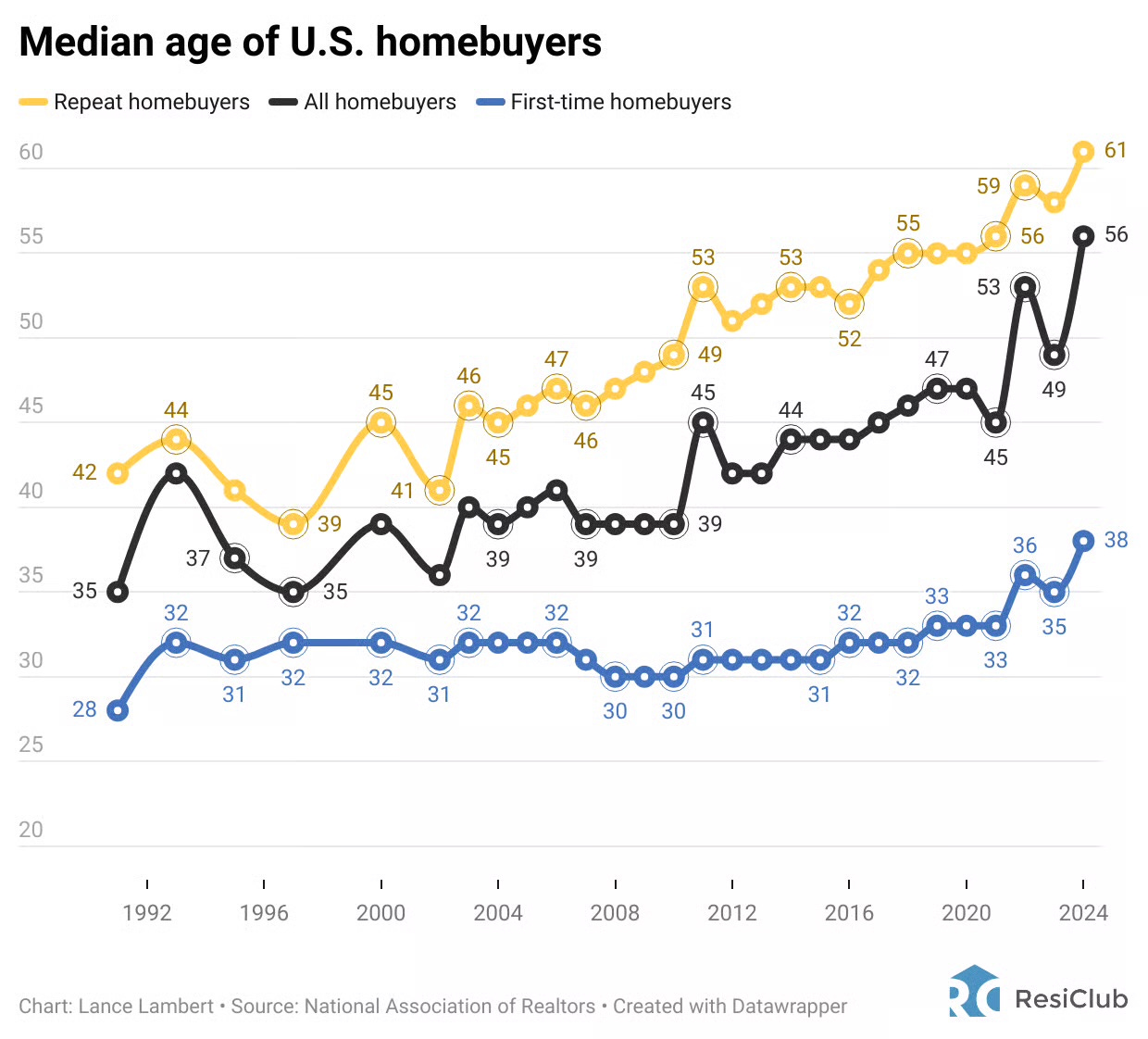

Indeed, until recently, it was common for couples in their mid-20s to buy their first house. Today it’s a rarity. In 1991, the median age of first-time homebuyers was 28. Now it’s 38, according to the National Association of Realtors. That’s an all-time high. In 1981, the median age of all homebuyers was 36. Today, it’s 56—another all-time high. This is the hardest time for young people (defined, generously, up to 40!) to buy their first home in modern history.

Beyond his statistical accuracy, it is Carlson’s anger—A TOTAL DISASTER!—that rings most true. Housing is so much more than a statistic. Our homes are our lives. Where we live shapes who we meet, what we do, and who we become. It is no coincidence that, as homeownership among young people has declined to all-time lows, marriage rates and fertility have also continued to plummet. Young Americans are the most depressed generation when it comes to the state of the economy. One might feel tempted to write this off as an extension of youth mood disorders, and persnickety economists can point out that young people today are not poorer than previous generations. But there is no debating the fact that today’s 20- and 30-somethings are significantly more blocked from owning a home than any other generation.

In the 1990s and 2000s, one’s 30s were a decade of ownership. Now, our 30s are a decade of mostly trying and failing to own. It is hard to capture in official government statistics what that kind of disappointment can do to the psyche of a generation.

A 50-Year History of the Housing Crisis

The deterioration of housing affordability in America, especially for young people, isn’t a simple story, but rather a nested history of troubles. There’s the 50-year tragedy, the 20-year tragedy, and the 5-year tragedy.

The 50-year story is significantly about rules. As Ezra Klein and I wrote in Abundance, the 1970s marked a turning point in the use of zoning restrictions. In prior decades, zoning had mostly been used to cut up cities and towns into business and residential zones, which often had the effect of keeping non-white and low-income people away from high-income neighborhoods. But in the 1970s, city planners and neighbors aggressively sought to restrict overall housing growth, through the expansion of exclusionary zoning, finicky rules like minimum lot sizes and parking mandates, and the normalization of NIMBY movements and lawsuits designed to block new development. "The 1950s and 1960s were a golden age of new construction," the economists Edward Glaeser and Joseph Gyourko wrote in a recent paper on the modern history of housing. But in the 1970s, construction rates plummeted. “In the 1980s and 1990s, the growth rate of housing was barely half the rates seen in the 1950s and 1960s.”

The 20-year story adds in the economics of homebuilding. The Great Recession of 2007 and 2008 obliterated the construction industry. Bankruptcies bloomed, and national construction employment fell by roughly 40 percent by 2010. Homebuilding was stuck in a depression for years, and the U.S. built fewer homes per capita in the 2010s than any decade on record. By 2019, home construction had slowly normalized, but since the large Millennial generation was rounding into their 30s, the prime home-buying years, a groundswell of demand pressure pushed home prices to new highs. Even as young people were earning more than their Gen X peers, many of them felt further from the promise of adulthood, as housing prices outran their raises.

The color-coded maps of Harvard’s Joint Center for Housing Studies make the point starkly. In 2000, most markets had a price-to-income ratio under 3. That means the typical price for a single-family home cost less than 3 years’ income. By 2022, the price-to-income ratio across the country had doubled. For all the economic and scientific advances of the 21st century, the last quarter century has been the period when the typical American had to work twice as hard to buy a house where they lived.

The 5-year story might be the most important in explaining why, when you look back at the first graph in this piece, you can see the median age of first-time homebuyers lurching in the last few years. If the 50-year story is mostly about the law, and the 20-year story pulls in economics, the 5-year story tops it off with virology.

The COVID pandemic shut down much of the service sector. But the home-buyers market was supercharged. Shut inside their homes, wallowing in cabin fever, and having nothing to do all day but stare blankly at their phones and daydream on Zillow, many couples sprang for bigger homes, often just outside major cities. Suburban home prices launched into the exosphere. Meanwhile, the construction market on the supply side was significantly slowed with shutdowns and supply-chain hardships. When the unstoppable force of pandemic housing demand smashed into the immovable object of supply-constrained homebuilding, prices went bonkers, if I may employ a technical term. Between March 2020 and the summer of 2022, the Case-Shiller U.S. National Home Price Index increased by 42 percent—equal to the entire home price index increase between 2003 and the beginning of the pandemic. In other words, the U.S. warp-speeded through two decades’ worth of housing inflation in about two years.

The worst part for young homebuyers had yet to come. Overall inflation surged in 2021 and 2022. The Federal Reserve raised interest rates to cool the hot economy. The typical 30-year mortgage rate jumped from about 2.5 percent in early 2021 to 7 percent by 2023, where it's hovered for the last two years. As a result, the typical monthly mortgage payment on new loans has more than doubled. (Meanwhile, insurance costs and tax payments on homes also rose, due to a variety of factors, including an uptick in natural disasters.) Higher rates don't just push housing costs out of reach for young middle-class couples. They also discourage homeowners with old mortgages from moving. After all, who would trade a 2.5% 30-year mortgage for a 7% 30-year mortgage if they didn't have to? As a result, existing home sales plummeted 20 percent between 2022 and 2025, falling to a 30-year low.

For young homebuyers in many places, it’s the worst of all worlds. Home prices are too high; and mortgages are too expensive; and insurance costs are too high; and existing homeowners don’t want to move; and all of this happened after decades of construction struggles and half a century of onerous rules and legal norms that blocked development in major cities. The 5-year, 20-year, and 50-year histories of the US housing market fit inside each other like a cursed nesting doll.

Toward a Housing Abundance Agenda

Housing has forever been integral to American life. It has more recently become core to American politics. I have seen private Democratic polling showing that young voters, who once considered housing the 20th or 25th most important issue facing the country, have recently put it in the Top Five. Housing affordability is now as essential to voters under 40 as protecting Social Security is to voters over 60. And politicians that recognize this fact will have a major advantage. In New York City, Zohran Mamdani shocked the establishment by running a campaign that was laser-focused on addressing cost-of-living issues (even if I disagree with some of his approach). After the 2024 election, the pollster David Shor found that the "single most effective" Kamala Harris ad had been her promise to lower housing costs by building more homes.

Donald Trump won a cost-of-living election. He had an opportunity to be the cost-of-living president. Instead, he has responded to America’s housing shortage with his own scarcity agenda. Rather than make it easier to build homes, he has announced tariffs on critical inputs, like Canadian lumber and Mexican drywall. His immigration crackdown tightens the labor pipeline for homebuilding, which relies on foreign-born workers more than almost every other industry. Rather than calm bond markets to help reduce long-term interest rates, he has signed off on a debt bomb of a bill and made noises about firing the chair of the Federal Reserve.

An abundance agenda for housing at the national level is possible. But it must begin with an appreciation for the fact that housing policy is exquisitely local. American cities and suburbs will need more wins like California’s recent CEQA reform, which will hopefully accelerate the construction of urban “infill” units. But Washington can urge this winning streak along. The federal government could experiment with a “carrots, not sticks” approach by creating a national rewards program that sent significant infrastructure and development funds to the states and cities that increased their housing permits the most. This YIMBY Carrot strategy wouldn’t just reward good behavior; it could also scramble the political psychology of local housing advocacy. Pro-housing groups would have a new counter for their NIMBY neighbors: “Hey, your opposition to new development is directly costing us money we could spend on parks and schools!” Or, “When you say no to new housing, you’re not just saying no to future residents, you’re taking money away from the people who are here now!” Meanwhile, reducing long-term mortgage rates is not a simple task. It will require that the US combat inflation in the short run and constrain our debt in the long run. Unfortunately, both are hard and neither is happening under this administration.

This essay has been full of catastrophic statistics. But an upside of catastrophe is that it gets people’s attention. America’s housing crisis has until recently roamed just outside the main radar screen of national politics. Today, housing is firmly at its center. Young people are voting on it. The news media is talking about it. Politicians are piecing together policies to address it, and even once-sclerotic blue states, such as California and New York, are finally acting on it. If Democrats want to remodel themselves as protectors of the middle-class, defenders of the American Dream, and stewards of a future that young people can believe in and afford, they have to come home to housing.

Sentence could end here.

As a 39-year old in a DINK household in the low six figures, everything in this feels true to me. We have no shot of owning a similar apartment in our neighborhood to what we currently rent.

I’m also skeptical of the “carrots, not sticks” approach. It reminds me of the early years of Obamacare when red states flat-out refused to take the federal dollars for Medicaid expansion. Their citizens suffered, and their leaders paid no political price for it. Never underestimate what a Long Islander is willing to pay in opportunity cost to keep their town/village/hamlet single-family and ethnically homogeneous.

(Edited for typos)

My house now (that no one would call a McMansion) is bigger than the house I grew up in, which is bigger than my grandparents’ house etc. (my grandmother lived there until she died in 2023 at age 94). Similarly, I saw a TikTok about a guy saying people complain about housing prices - but for example, he grew up without air conditioning in his house. Serious question - do these stats take those kinds of things into account? I never know that when I read these articles. Thanks! P.S. Ramit Sethi suggests renting and investing the difference as the mathematically better investment over buying a house if anyone wants to check him out.