‘Yes, AI Is a Bubble. There Is No Question.’

The evidence that artificial intelligence is a big fat bubble has, confusingly, gotten much stronger and much weaker at the exact same time.

The funny thing about unprecedented events is that they tend to evoke the strongest reactions, even though, by their very nature, unprecedented phenomena have no track record that clearly points us toward a likely outcome. So it is for artificial intelligence.

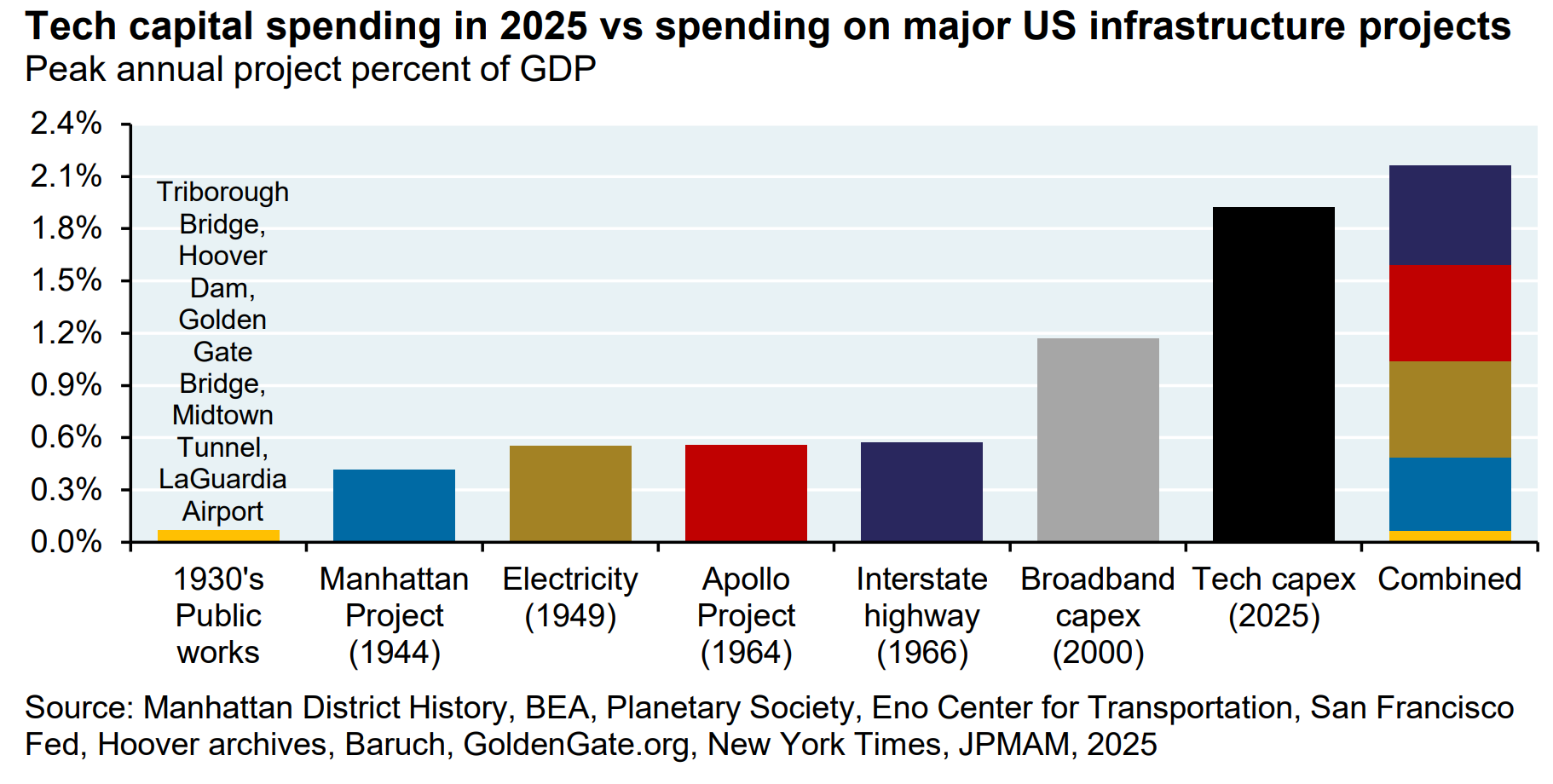

What you’re seeing in the remarkable chart above is that private sector spending on AI in 2026 is forecast to exceed $700 billion, which is not a number that is easy to think about. As a share of GDP, companies are currently devoting more resources to AI than the combined peak annual capital spending on key 1930s public works projects and the Manhattan Project and the 1940s electricity boom and the Apollo Project and Interstate highway construction. It’s important to note that AI spending is overwhelmingly financed by the private sector, whereas most of those infrastructure projects were financed by the largesse of the federal government. Once again, nothing like this has ever happened before, and if you feel extremely confident about how this is going to turn out, I think you might be crazy.

Alas, when one’s chosen profession is writing essays and making podcasts and generally presenting oneself as a pundit, comfy ambivalence gets you absolutely nowhere. So, rather than stick to one extremely boring yet honest message—I’m uncertain about the future—I’ve tried to stake out falsifiable predictions about AI, at the risk of changing my mind often. Six months ago, my strongest feelings about the future of AI hewed closely to a framework articulated by the economist Carlota Perez. In her book Technological Revolutions and Financial Capital, Perez showed that general purpose technologies tend to produce economic bubbles before they produce technological revolutions. Whether it’s the canal mania of the first industrial revolution, the transcontinental railroad of the 19th century, or the dot-com bubble of the early 21th century, the beats of the story are as familiar and predictable as a Save the Cat story arc. Once upon a time, Shiny New Thing is born. Speculative capital pours in. Companies get so excited about the prospect of Shiny New Thing that, failing to coordinate their spending to perfectly match forthcoming demand, they overbuild. The Shiny New Thing bubble pops. Then productive capital takes over. Firms learn to use Shiny (Not So) New (Anymore) Thing. As the technology diffuses throughout the economy, a golden age of broad and steady growth follows. One of Perez’s core insights was that bubbles and golden ages are not a one-or-the-other kind of thing. They often arrive in sequence: one, then the other.

Riding the coattails of Perez, I was very certain that AI was a bubble, for the simple reason that I thought AI spending was rising faster than revenue could possibly match it. But in the last few weeks, I changed my mind. And I want to be very clear about what changed it.

In late 2025, the AI companies Anthropic and OpenAI released new agents—that is, AI that can work autonomously on complex projects that require multiple stages of reasoning. These agents became so popular, so quickly that Anthropic’s revenue doubled in two months, and OpenAI reportedly added one billion dollars in annualized revenue per week in the last few months. At this rate, these are two of the fastest growing companies of all time. And the AI revenue surge is not just at two frontier labs. The payments firm Stripe, which has a god’s-eye view of thousands of companies on its platform, has said that AI companies are growing revenue faster today than any other generation of companies they have ever seen.

The Perez bubble story suggested that general purpose technologies always build too fast while revenue comes along too slow. But the AI 2026 story seems like a rare exception: A historic rate of spending coinciding with a similarly historic surge of revenue.

As my confidence in the AI-bubble narrative weakened, I wanted a gut-check. Last year, I interviewed the investor and writer Paul Kedrosky, and it was hands-down one of the most popular interviews of the year. So, last week I called Paul and said: Try to convince me again. This interview is absolutely jam-packed. In an hour, we somehow cover:

Why the biggest tech companies, after dominating the stock market in 2024 and 2025, have had such a rough start to 2026

The omen of the “Saas-pocalypse”—the sharp decline in stock prices for several publicly traded software companies

The growing private credit crisis, explained

Why the enormous revenue boom from new agents like Claude Code might be a sugar high, in which explosive revenue growth today precedes much slower revenue growth after AI adoption among software engineers peaks

If equity value is flowing if it’s leaving software

Why productivity might seem to be rising (“The reason has nothing to do with AI,” Paul says.)

Below is a polished transcript of our conversation, organized by topic area.

‘WE’VE NEVER HAD A MOMENT LIKE THIS’

Derek Thompson: In a nutshell, what is the 2026 Paul Kedrosky thesis for why AI is a bubble?

Paul Kedrosky: AI is a bubble because it’s one of the probably five largest CapEx bubbles in history, meaning that at this moment where we’re building out infrastructure like canals, like railroads, like rural electrification, like fiber optics, where we’re building out this huge new substrate on top of which a lot of economic activity happens. And this is a particularly large example of that, to the point that it’s a material fraction of GDP growth, like 50 to 80% depending on the quarter and whose numbers you use. And these things inevitably lead to a series of rotating crashes as we overbuild and the assets become unable to pay their way with respect to the debt that’s used to finance them. And then there’s a big reset and then we maybe find another use for them. This happened with fiber, this happened with rural electricity, this happened with railroads, this happened with canals.

And if it didn’t happen this time, it would truly be the first time in modern economic history — which isn’t the same thing as saying that AI itself is somehow frivolous or useless. AI is an incredibly important technology. Saying that we’re in an infrastructure bubble is not the same thing as saying that these large language models don’t work, or they’re just autocomplete or whatever. These are two very different arguments.

And this particular moment is unique because it combines all of the things that we found in prior bubbles — loose credit, real estate, technology, government policy. We’ve never had a moment like this with a huge infrastructure buildout at the intersection of all four of the things that have caused the most consequential infrastructure bubbles in U.S. history. Every one of the actors feels like they’re acting in a rational way — “I don’t know what those guys are doing in technology, but we here in real estate, we know what we’re doing. And whenever we sign a lease contract to a hyperscaler, we know we’re looking at a prime credit.” So the consequence of all these rational actors is what finance theorists call a rational bubble — where the intersection of rational actors produces something that’s economically indefensible.

Thompson: The analogy you’ve given so often is the railroads. What was the lesson of the railroads?

Kedrosky: Railroads were a very good idea. They weren’t Beanie Babies. They were really important, and on top of them we did a lot of important economic activity, not least of which was settling the Western United States. But that didn’t prevent people from over-funding startup railroads such that roughly half of the track miles built at peak periods in the mid-19th century were eventually abandoned. Does that mean railroads were a bad idea? No. We just wildly overbuilt, because the impulse to build was so imperative that everyone building railroads felt like there’s an opportunity to be an oligopolist here — “When all of this shakes out, I’ll be the consolidator.” Which is a very similar impulse to what we hear today. Dario Amodei said this recently, that there will only be one or two, maybe three players at the end of all of this. And it leads to misaligned incentives — “I don’t mind that what I’m doing right now isn’t paying off, because over time I plan to be the consolidator.”

And the other lesson, which I think is particularly striking, is that people have forgotten not just that there was all this redundancy, but that the railroad buildup led to a series of financial crashes in the 1870s — the crash of ‘73, crash of ‘78, crash of ‘87 — each of which killed off a significant number of companies and financial institutions. Nevertheless, in 1900, railroads were roughly 62% of the index market capitalization in the United States. They were the technology company of their time. So building out that platform was rewarded, but was also consequential in terms of leading to various financial crises — and it played a secondary role in the Great Depression itself.

None of these things mean that railroads were a bad idea. But the carnage along the way was dramatic. The metaphor for me is that you can have a hugely valuable buildout that is really consequential for decades in terms of both productivity and economic and financial carnage.

Strikingly, technology writ large is around 60% of the all-U.S. index today. So you’re in a similar situation — this industry has grown to remarkable dominance of the broader equity indices, much like the railroads did. And much like the railroads, it’s become increasingly capital-intensive, which has consequences for how investors are looking at technology companies now versus the halcyon days of the 1970s.

Thompson: For folks interested in going a little deeper on the railroad analogy, we did a podcast with Richard White, the Stanford historian who wrote a wonderful book called Railroaded. His thesis is that the Transcontinental Railroad was a technology built by corrupt idiots working in concert with craven politicians, which led to one depression after another, panic after panic, inflation, deflation, crashes of the economy — and it was a good idea and it completely transformed the country. You can have yes, no, no, yes answers to the questions “Is it a bubble? Was it built by idiots? Is it important?” because they are profoundly different questions. Sometimes bad people in the process of crashing the U.S. economy over and over again nonetheless build technologies that in the long run we can’t imagine modern life without. It’s a strange, amoral feature of history.

Kedrosky: I completely agree.

WHY IT’S A BUBBLE, PART 1: THE HYPERSCALERS’ DILEMMA

Thompson: A lot’s changed since 2025 when we spoke, and I think some of those changes validate your prediction, and some complicate it. Do you still think that AI is an industrial bubble right now?

Kedrosky: Yes. AI is a bubble. There’s no question.

Thompson: Why?