This War's Economic Crisis Could Get Much Worse—For the U.S. and the Whole World

This isn't just about the price of oil. It's about everything oil becomes—fertilizer, AI chips, plastic—and the cost of snapping the achilles heel of the global shipping economy

Today’s post is about the economic fallout of the Iran War, which—depending on the hour that I check the news—is either about to end, or just getting started, or already achieved its objective, or requires a ground invasion. Uncertainty in war is no novel phenomenon. The 19th century Prussian officer Carl von Clausewitz is widely credited with popularizing the concept of war as a “fog.” But one might have hoped that two centuries later—with the invention of computing, advanced analytics, the Internet, and a vast network of global surveillance—that proverbial fog might have lifted. Instead, I have found it immensely challenging to track the war on a moment-to-moment basis given the avalanche of partially accurate, fully inaccurate, or deeply misleading information from reporters, analysts, and even our own government. On Tuesday afternoon, Secretary of Energy Chris Wright posted that the US Navy was escorting tankers through the Strait of Hormuz … and then minutes later deleted the post after a reporter questioned the claim.

Today I wanted to pull back the lens and share a conversation I had with a geopolitical energy expert on the global economics of this war—why the near closure of the Strait of Hormuz is such an enormous deal for the entire world and why energy crises tend to have such wide ripple effects.

What do the following things have in common: the death of the Soviet Union, the rise of modern conservatism in America, and Nintendo? Answer: An energy crisis.

In October 1973, Arab members of OPEC launched an oil embargo against the United States and its allies. Within months, the price of a barrel of crude quadrupled. In the U.S., the immediate effects included gas lines and a national speed limit. A second shock followed during the Iranian Revolution of 1979, and gas prices surged again. The combined effect was the toxic union of stagnation and inflation, two things that economists had previously said were practically incapable of coexisting. The immediate effects — gas lines and recession — were the least interesting consequences of this historical event. The arms of the crisis reached around the world:

In the USSR: Oil shocks were a windfall for the Soviet petroleum economy, and oil money allowed Moscow to paper over the dysfunction of its planned economy for years. But in the 1980s, oil prices fell, and Gorbachev’s petro-economy collapsed, contributing significantly to the demise of the Soviet Empire.

In Japan: Heavy industry, relying on cheap oil, had powered the economy in the 1960s. But expensive oil threatened that model of growth. In the 1970s, industrial policy was rerouted toward smaller manufactured goods that required less energy: computer chips, circuits, and robotics. The consumer electronics revolution of the 1980s in Japan—the Walkman, the VCR, Nintendo—was an echo of the oil crisis.

In the United States, the historian Gary Gerstle has described how stagflation shattered the New Deal consensus. Americans lost faith in the sort of activist government associated with Roosevelt, Truman, and LBJ. The political order that emerged from this period prized individualism, celebrated markets, and outwardly mocked the idea of effective governance. The election of Ronald Reagan, and thus the rise of the modern conservative movement, is hard to imagine in a world where the economy of the 1970s is as copacetic as the economy of the 1950s.

So, there you go: perestroika, Nintendo, and Reagan. None of these things were entirely caused by the energy crises. But in each case, the oil shocks of the 1970s reshaped the political and economic environment in a way that increased the odds of the collapse of the USSR, Japan’s shift toward electronics, and the demise of the New Deal order.

The vast and sprawling tentacles of past energy crises have been on my mind recently during the Iran War, which has shut down most commerce passing through the thin Strait of Hormuz. It would be reckless to predict precisely where this conflict is headed. But it no longer seems reckless to say that this war is going to be a mess: if not just a military mess, or a diplomatic mess, then at least an economic mess. The vast majority of headlines in the Wall Street Journal and Bloomberg are about the price of crude oil. But the deeper story is about everything crude becomes, everything that moves alongside it, and everything that depends on the narrow maritime chokepoint at the mouth of the Persian Gulf.

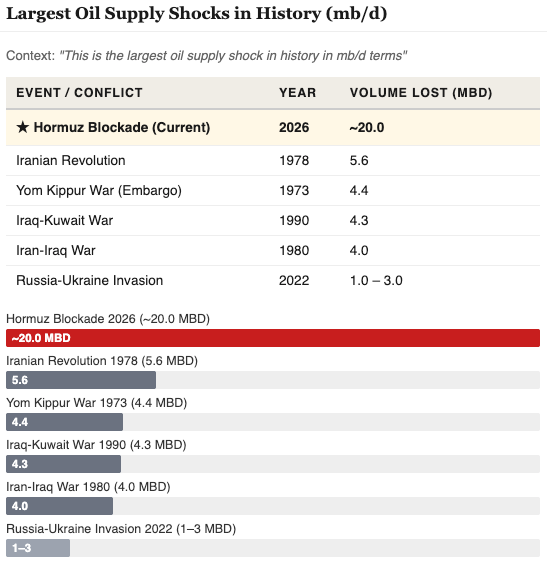

The Strait of Hormuz is the global economy’s ACL: a small and vulnerable connective tendon that you don’t have to think about when it’s working perfectly and causes very loud anguish when normal function is ruptured. By some measures, the Iran War is already the largest sudden disruption of oil supply in modern history. If this conflict continues to disrupt traffic through that passage, the consequences will not stop at gasoline prices. They will spread into fertilizer, petrochemicals, plastics, jet fuel, shipping, power markets, and manufacturing supply chains that most people never think about until they seize up.

Before the war has reached its second birthday in weeks, the signs of disorder are everywhere. Energy facilities have come under direct attack. Production has been cut back in parts of the region. Qatar has declared force majeure on liquefied natural gas exports. Governments in Asia are already beginning to respond with emergency measures to conserve fuel and electricity. In just the last few days, Vietnam has reportedly urged people to work from home to save fuel; Myanmar’s junta reportedly launched a rationing system for cars; Thailand restricted fuel exports; and the Philippines prohibited air conditioning settings below 75 degrees in government buildings and instructed officials to turn off their computers when they go to lunch.

To understand what is happening, and why the fallout from this conflict could extend far beyond oil itself, I talked to Rachel Ziemba, one of the sharpest analysts of global energy markets and economic statecraft. We discussed:

Why the Iran War economic fallout goes far beyond gas prices

Which countries and regions will feel the most pain

Whether a swift end to the war will swiftly end the economic crisis that the war triggered (probably not)

GASOLINE, JET FUEL, FERTILIZER, PLASTIC, CHIPS…

Derek Thompson: Tell me about the Strait of Hormuz.

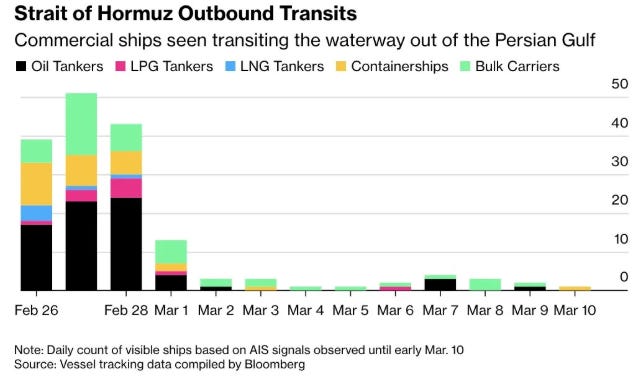

Rachel Ziemba: The Strait of Hormuz is a narrow strip of water between the United Arab Emirates and Iran, through which more than 20 percent of global oil transits, 20 percent of seaborne liquefied natural gas, 30 percent of seaborne fertilizer, and a growing amount of global container traffic. I’ve been tracking energy markets and the Middle East for about 20 years. Even before that, as a grad student, we studied chokepoints and physical risks to energy markets. The Strait of Hormuz has always been number one. But this is the first time it has been effectively blocked, and there hasn’t yet been a way to reopen it.

Thompson: From news headlines, this sometimes seems to be only a story about oil. But I prefer the idea that this is a story of what oil becomes, and how it’s a universal input in the global economy. What does oil become?

Ziemba: As consumers, we don’t use oil. We use gasoline. We use diesel. We might get on a flight and hope that it has jet fuel. In the massive buildout of electricity, because of AI, we use copper. To process copper, we use sulfuric acid, which is a byproduct of oil refining. In our daily lives, we use plastics, which come from petrochemicals. Oil and natural gas can also be precursors to fertilizer, nitrogen-based fertilizer in particular, which can add to the costs we face in our food supplies.

Think about it this way: I placed an Amazon order this morning. The car that’s going to handle that last mile, the flight it’s on, all of those involve companies that are thinking and scrambling about whether their costs increase. Even the ships the oil is being carried on are themselves having to pay more for fuel. So it really has a number of ripple effects in the global economy.

Thompson: Since we hear so much about the price of a barrel of oil, I want to go deeper into some of the other affected products, especially fertilizer and computer chips. I’ve read that up to 40 percent of global urea shipments from the Middle East are essentially stranded right now outside the Strait of Hormuz. What’s the connection between the strait, oil, and fertilizer use throughout the world?

Ziemba: Urea is one of the formats in which [hydrocarbons] can be converted into fertilizer. It can be a byproduct from natural gas or oil that is then converted into nitrogen-based fertilizers. It’s one of several sources of fertilizer, along with phosphates and potash. Major suppliers of phosphates and urea are trapped in the strait, with the producers of Saudi Arabia and Qatar respectively.

We’re already seeing a price impact even here in the United States. I looked at prices out of the Port of New Orleans today, and they’re now, I think, $270 a ton. That’s up 77 percent since December. So if you’re a farmer who is thinking about the cost of fertilizer versus what you can sell corn for, that matters.

Here in the U.S., most of the fertilizer we import comes from Canada. About 40 to 45 percent is potash coming in from Canada. There are no supply shortages there. Another roughly 20 percent comes from Russia. At this point it is our only primary import from Russia in the context of sanctions, at least for now. We’ll see what happens later this week. But still, this is a case where fertilizer costs will be going up, and this also comes at a point when other inputs going into farm products may be affected by tariffs and uncertainty around tariffs.

Thompson: On computer chips: Taiwan makes about 90 to 95 percent of the world’s most advanced chips, and Qatar ships about 30 percent of [its liquefied] natural gas through the Strait of Hormuz. South Korea is making noises about fearing that helium shipments could be slowed, and helium is a major input for Korea’s memory chips. So: no gas, no helium, no power, no chips.

Ziemba: People are rightly worried about this shortage of helium. Some would point to the fact that the U.S. was among the countries that sold off its helium reserve, in part because we don’t do as much semiconductor manufacturing in the United States, though that is shifting.

Taiwan faces a triple whammy: concern about power supply, power being more expensive, and concern about other inputs [such as helium]. This is happening at a time when memory chip prices have already been going up sharply. That was partly a story of really strong demand, as AI-related inputs and imports have been going up in the United States and around the world.

It’s not only a data-center issue. Memory chips are used downstream in building cars. We saw in the pandemic that if auto manufacturers canceled their orders for chips, they might end up at the back of the line because they weren’t as large an orderer. So we could see this filtering through into a range of other manufactured products.

Ultimately, you’re also pointing to the question of which products are stockpiled and how easy it is to have stockpiles. Any time you have a stockpile, that means buying a product you’re not going to use immediately and having it ready in case there is a shortage. This is the opposite of just-in-time manufacturing. When we look around the world, some countries, like China and even the United States, have large oil stockpiles, but very few countries have large natural-gas stockpiles. That is something I anticipate will be rethought.

Thompson: So, with the shutdown of the strait, oil prices are going up, but really it’s about about the stuff we make from oil going up in price. Sulfuric acid is how we extract copper. Copper is what we use to make transformers and electric vehicles and all parts of the green-energy economy. We’ve got plastics. We’ve got helium that’s stuck behind this closure. We’ve got fertilizer. So, the agricultural economy, the chips economy, the plastics economy, the green-energy economy—all of these different sectors of the U.S. and global economy are being affected by this closure.

Ziemba: Spot on. In a political context, gas prices going up tend to be the trigger and warning sign. But if we look at it, the impact on the U.S. and global economy is much greater. If anything, it’s really going to drive differentiation between countries.

There may be countries like China, which has a very large crude oil stockpile it has been adding to when prices were low, that might be able to subsidize parts of its plastics or petrochemical production. That might make them even more competitive even as they hold off on exporting refined oil products. We’ll see how that plays out. But I think we could see differentiation on competitiveness that might further challenge onshoring and reshoring goals that are underway here in the United States and elsewhere.

HOW IT ALL ENDS

Thompson: How do you see the Iran War ending?